When to take VC

It may be a surprise to hear this from a venture capitalist, but the vast majority of startups should not take money from our industry. The history of entrepreneurship is the history of owner-managers with no outside shareholders. Indeed the data shows just how few startups take venture capital - one in every 2,000 startups in the US.

Few entrepreneurs start off with crazy aspirations to invent a new market category, or hollow out a multi-billion dollar incumbent. Most simply want independence, to build a proprietorship that is theirs. These startups should either take no outside funding, or perhaps small investments from friends and family. In fact, friends & family and personal savings account for 11x amount of capital in startups as VC provides.

Sometimes founders discover that the market opportunity (and maybe what they discover about their own abilities) opens up much larger vistas, and at that point they may consider outside capital to fuel their plans.

A tiny subset of this group of startups work so well that they grow into big businesses without significant external capital. They are in the luxurious position of having the choice of raising capital at any stage - from venture firms on the way up, and later from growth or private equity funds. We at Mosaic would be happy to partner with founders of such businesses early, not because they need our capital but because they want true partners as they scale their business over many years.

The final group comprises the minority of businesses for whom raising venture capital makes sense to fuel their ambitions. Across European tech today, we count over 2,000 startups funded by seed investors annually and in 2015 there were roughly 325 startups that went on to raise Series A from a VC.

So when should a startup consider taking a first venture round from an early stage fund like Mosaic?

Here are some simple filters for the entrepreneur:

1. The startup should address a very large market (billions of dollars).

2. You should have immense ambition. At Mosaic we talk about mission driven entrepreneurs, who are not mere mercenaries; who have chosen a mountain to climb and are determined to conquer it. That mission is worth some of your best years.

3. You are committing to a liquidity event at some point in a 8-10+ year horizon - this is a different path to a proprietorship. Many founders welcome this because they have employees with shares or options, or already have other outside investors who expect some form of liquidity event too. The liquidity event could be a sale, or IPO to monetise stakes held by investors and staff, or even a partial sale (e.g. of a VC stake to a private equity firm). The best VC funds wait patiently for the right moment to sell; nevertheless taking VC means that the entrepreneur will need to provide a path to liquidity at some point.

4. The size of fund you take money from helps to define the investor's ambition for the liquidity event. Fund maths is straightforward: $500 million funds seek an outcome of $750 million - $1 billion, as if they own the proverbial targeted 20% of a company at exit, the $150-200 million return is meaningful in the context of their fund. As a $140 million fund, at Mosaic we invest believing that, if successful, each investment we make ideally should have a shot at returning the entire fund. Failing that, we'd hope there is at least a reasonable shot at returning something like $50-75m, or a third to half of our fund. For Mosaic, assuming a stake of 10-20% at exit, the company needs to be worth $250-500 million or more.

And whatever the aspiration of the investors, alignment with the entrepreneur's goals is paramount. The journey is too long and has too many pitfalls to add friction by having investors that are either a constraint or structurally likely to be dissatisfied.

5. The entrepreneur should be clear what sort of relationship they want with their VCs. This has two aspects.

First, the nature of the support you expect to receive and that the VC is able to give. Some experienced entrepreneurs might prefer a somewhat passive investor; we have made such investments before where appropriate. Often, entrepreneurs want more, and we enjoy being a sparring partner to anticipate, debate and inform the big issues. We are on your side of the table but in that context, we challenge entrepreneurs on why they are taking certain decisions. We back the entrepreneur to make the final call, but we hope to earn sufficient trust so that - where we can justify our views - they are heard, and the debate is real.

Second, there is also an intangible aspect, of chemistry, to consider. Your lead venture investor will be an integral part of building your business over several years. You need to feel that the firm you choose has an ethos that works well for you. That relationship not only relates to the input you require but also the sorts of people you work well with. If the chemistry is wrong, it can get in the way of meaningful discussions at critical junctures - both with the individual partner and also the firm as a whole (if it operates as a firm). If it is right, it can help you get through harder times and resolve issues collaboratively and efficiently.

6. The entrepreneur has studied the market carefully, knows their (prospective) customers intimately, and can articulate simply how their startup will build a "moat" to win against serious competition. (We will discuss the pitch explicitly in a future blog.)

7. As an early stage fund, we expect most companies that we invest in to raise follow-on financing in due course. So the operating plan should deliver realistic milestones that enable the startup to raise more capital from good investors. The plan should include organisational buildout, especially key recruits; a compelling product roadmap; and commercial traction or some other compelling validation.

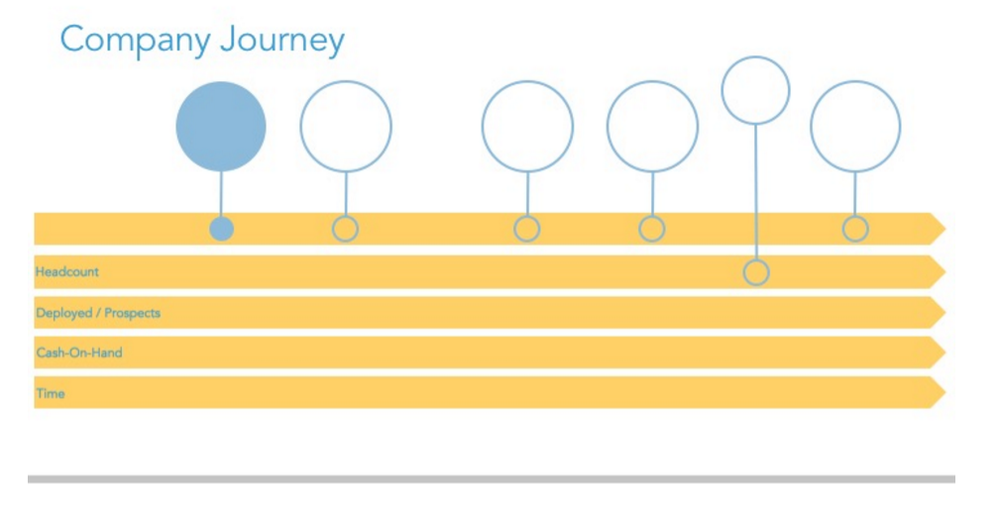

An example is the early plan put together by founder Andrew Rubin for enterprise security startup Illumio. It was summarised in just one slide and looked something like this, with major deliverables and milestones in the bubbles:

In any founder's journey, there are a lot of significant decisions to make, and few are as seismic as taking venture capital. We recognize building a business from the ground up is hard, and that taking VC funding sometimes commits an entrepreneur to a more aggressive path to value creation - and so to taking more risk. It can be a difficult road. So before you even consider a fundraise, carefully weigh up if and when it is right for your business, the market opportunity you have and be honest about your aspirations.

If VC is for you, please get in touch. Otherwise - grow your business methodically, take measured risks, be proud that you have no reason to take VC.